Tokyo operators

Tokyo-headquartered operators with US subsidiaries, keiretsu-adjacent firms, and technical B2B owners rebuilding the US website, deck, and sales material for category, outcome, and peer set.

Tokyo operators →For Tokyo-headquartered industrials, semiconductor and precision-electronics firms, medtech and cyber operators, and Japanese family-office-backed holdings entering the US. We rebuild the US category, buyer language, website, sales deck, and follow-up sequence so American buyers can place the company quickly.

The search is not academic. It usually means the firm has a credible Japanese position, a US target, and a fear that a direct translation will waste the first American push. This page now answers that exact moment.

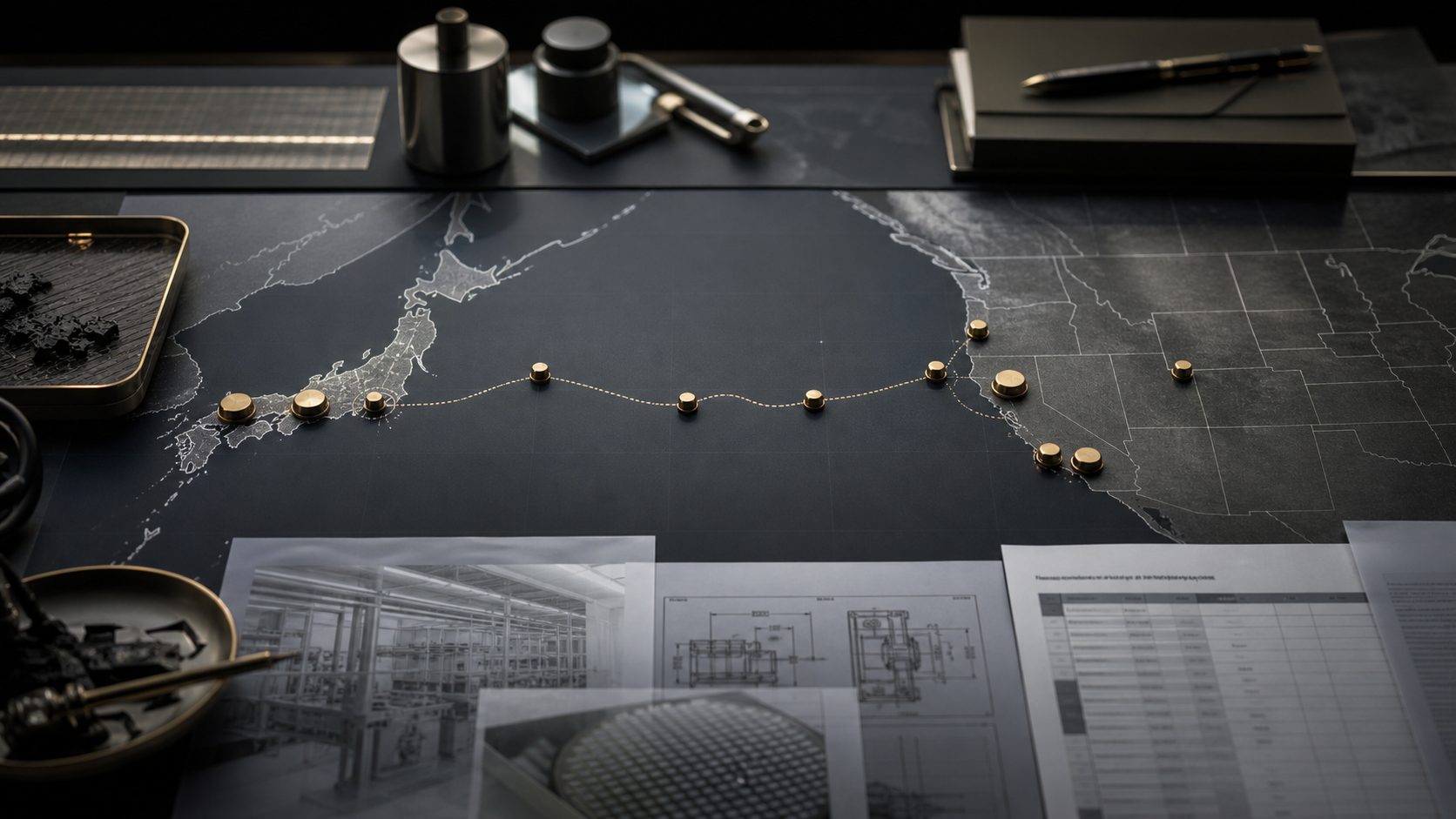

Start the US launch inquiry →The Tokyo business is real. Standing inside the keiretsu, the Mitsubishi or Toyota supply chain, the precision-electronics ecosystem, the medtech tier defined by Olympus, Terumo, and Sysmex, and the zaibatsu-descendant capital base has been earned through generations of process discipline, supplier accountability, and category leadership at global scale. Revenue is validated. The decision is made to put weight into the US market. A US subsidiary opens, a US distribution channel begins, a US procurement entry moves forward, a US co-investment runs, or a portfolio company starts its American commercialisation. The first ninety days do not match the model. US meetings happen. US follow-up goes cold.

The instinct is to lead with specification depth, defer to existing US peer hierarchy, avoid overclaim, and let the work speak. The instinct is right at home and wrong for the American buyer. Japanese commercial culture signals seriousness through restraint, consensus, and engineering depth. US procurement buyers, US co-investors, and US distributors evaluate the same emphasis as deference, missing commercial position, or technical-only output. The American buyer does not interpret restraint as authority. They interpret the absence of an outcome claim as the absence of a US position.

American buyers sort fast on three signals: category anchor, outcome claim, and US peer set. Tokyo materials tend to omit all three by design. Japanese firms are often the largest in their global category and arrive in the US evaluation as small. The work is to translate the Japanese identity into US-legible commercial visibility without flattening what carries at home.

The American buyer is not asking for less rigour. They are asking for the category, the outcome, and the US peer set. Tokyo firms lead with specification, defer to the US incumbent, and omit the rest. GMA market observation on Tokyo to US entry

The precision is not the problem. The category position is.

Tokyo-headquartered operators with US subsidiaries, keiretsu-adjacent firms, and technical B2B owners rebuilding the US website, deck, and sales material for category, outcome, and peer set.

Tokyo operators →The closest existing APAC corridors. Hong Kong family-office capital and Singapore industrial and fund-led operators rebuilding for US visibility through an Asia-anchored channel.

See Hong Kong corridor →The wider city map. Tokyo sits inside a multi-city APAC and global corridor architecture for operators entering US markets through a single firm.

See all city corridors →Six to ten weeks. Single US category, single corridor. GMA rewrites the offer, proof, price story, website, and sales material for the American buyer, then launches the work.

See the Sprint →Three to six months. Multi-channel US rebuild and run. Ads, website, search, sales pages, follow-up, and sales material. The standard shape for Tokyo owners committed to US scale.

See the Build →Monthly retainer, twelve-month minimum. Ongoing rebuild-and-run across multiple US website, deck, and sales materials. Typical for Tokyo industrial groups, keiretsu-adjacent operators, and family-office-backed portfolios with several US-facing brands.

See the Partnership →No legal services. No Japanese kabushiki kaisha or godo kaisha formation, no METI or FSA filings, no Japan-US tax-treaty structuring, and no US entity formation. No L-1, E-2, EB-5, or O-1 visa work. No US tax structuring, transfer-pricing analysis, or double-tax-treaty analysis. No US banking introductions. No fiduciary services. No regulatory licensing. No IP filing. No contract drafting. No M&A transaction work. No recruiting.

These belong with Japanese counsel who specialise in US entry, and with US counsel on the American side. The firm works inside the parameters they set. When a marketing decision carries legal or tax implications, the firm flags it and defers before execution.

Tokyo runs on keiretsu provenance, consensus-built decisions, and a specification register that is engineered to avoid overclaim. American buyers filter on category anchor, outcome claim, and US peer set in the first scan. The Japanese restraint that signals seriousness at home lands with a US procurement buyer, US co-investor, or US distributor as deference, technical-only positioning, or absence of commercial position. The firm does not change at the border. The buyer does. The correction is buyer-language translation, not identity replacement.

Industrials inside the keiretsu and Mitsubishi or Toyota supply-chain adjacency, technical B2B in semiconductor and precision electronics, medtech in the Olympus, Terumo, and Sysmex adjacency, cyber operators in the NEC, NTT, and Fujitsu adjacency, engineering-commercial firms, and zaibatsu-descendant family-office capital with US-bound holdings. The firm also works with Japanese operating-company US subsidiaries already running. Fit is checked against the concrete US move, not published sector lists.

No. Japanese kabushiki kaisha or godo kaisha formation, METI and FSA filings, Japan-US tax-treaty structuring, US LLC or C-corp formation, L-1, E-2, EB-5, and O-1 visa support, transfer pricing, US tax residency, and US banking introductions are handled by the owner's Japanese counsel and US counsel. GMA builds the US website, deck, proof, and follow-up around the legal and tax structure counsel already chose.

As a structural advantage that has to be made visible in US terms. Japanese firms are often the largest in their global category and arrive in the US evaluation as small. Keiretsu provenance, supply-chain depth, and zaibatsu-descendant capital carry weight at home that is invisible to a US procurement buyer without translation. The work is to anchor the US category, name the outcome, and place the firm against a US peer set the buyer already trusts, without flattening the Japanese provenance that earned the standing in the first place.

With an inquiry through the contact form and an initial fit call. The firm runs three engagements: Market-Entry Marketing Sprint (6 to 10 weeks), Cross-Border Marketing Build (3 to 6 months), or Global Marketing Partnership (monthly retainer, 12-month minimum). GMA confirms fit and pricing after the initial fit call. Public prices are not listed.

The pillar piece. How keiretsu-adjacent industrials, Korean technical B2B, and broader APAC operators rebuild the US website, deck, and sales material for category, outcome, and peer set.

Open the pillar →The nearest existing APAC peer to Tokyo. Hong Kong family-office capital and operators rebuilding for US visibility through an Asia-anchored channel.

See Hong Kong corridor →Sprint, Build, and Partnership shapes. Which engagement fits a Tokyo industrial, technical B2B, or family-office rebuild for the US.

See engagements →The corridor splits into audience-specific routes. Open the route that matches the situation.